Learning Resources, INC, et al. vs. Trump: An analysis

By Avery Sneed ‘27

Introduction

In recent years, presidents have increasingly relied upon broadly worded statutory authorities to exhibit sweeping executive power to implement economic and regulatory policies. From pandemic responses, to student loan relief, to nationwide environmental regulation, the Executive Branch has asserted expansive power to address perceived national emergencies and urgent domestic policy challenges. As a result, the Supreme Court has had to respond in kind. In doing so, the Supreme Court developed the major questions doctrine, under which the Court requires the government to point to explicit congressional authorization that permits the sweeping executive action they intend to take. Although the major questions doctrine was originally designed as a check on the bureaucracy, its scope and implications for presidential authority have continued to evolve. The Supreme Court’s decision on Friday, February 20th, may have been the most impactful of any major questions doctrine analysis yet.

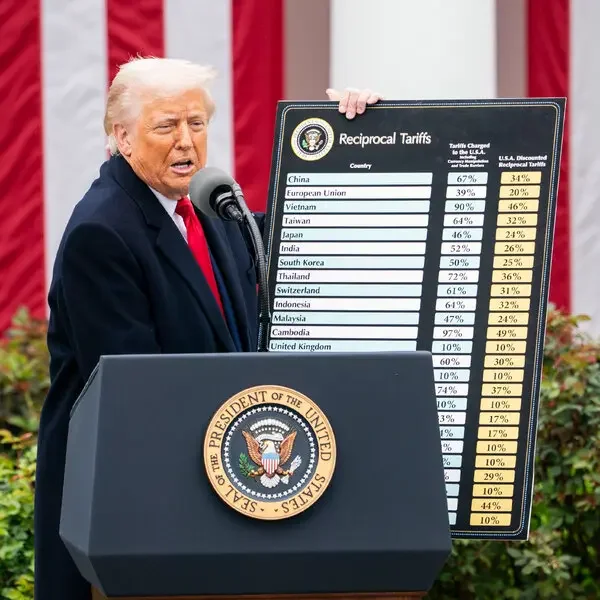

Shortly after assuming his role as president, Donald Trump sought to address two foreign threats: the alleged influx of illegal drugs from Canada, Mexico, and China, and “large and persistent” trade deficits. The President proclaimed that the influx of drugs (presumably fentanyl) had “created a public health crisis,” and the trade deficit had led to “the hollowing out” of American manufacturing and “undermined critical supply chains.” Subsequently, the President declared a national emergency as to both threats, deeming them “unusual and extraordinary,” and invoked his authority under IEEPA to respond. IEEPA, or the International Emergency Economic Powers Act, is a federal law enacted in 1977 authorizing the president to regulate international commerce after declaring a national emergency in response to “any unusual and extraordinary threat…which has its source in whole or substantial part outside the United States.” IEEPA authorizes the president to “investigate, block during the pendency of an investigation, regulate, direct and compel, nullify, void, prevent or prohibit…importation or exportation.” Absent this lengthy delegation of power to the president, however, is the power to unilaterally impose tariffs without restraint.

Even in the absence of such a power, the President imposed a dizzying array of tariffs under IEEPA. As to the threat from drug trafficking, the President imposed a 25% tariff on most Canadian and all Mexican imports, and a 10% tariff on most Chinese imports. As to the trade deficit tariffs, the President imposed a tariff of at least 10% on all trading partners of the United States. Since imposing each salvo of tariffs, the President has issued several increases, reductions, and other modifications with unimpeded discretion. This case was the result of a combination of two separate cases involving IEEPA challenges. First, petitioners in Learning Resources, two small businesses, who sued in the U.S. District Court for the District of Columbia. That court denied the government’s motion to move the case to the United States Court for International Trade, and granted the plaintiffs motion for a preliminary injunction, concluding that IEEPA did not grant the President the power to impose his tariffs. The plaintiffs in the adjacent case, V.O.S. Selections, were five small businesses and twelve states, who sued in the Court for International Trade (CIT). That Court granted summary judgement for the plaintiffs, and the Federal Circuit affirmed in part, holding that IEEPA’s grant of authority to the president did not include the power to tariff. The government filed a petition for certiorari in V.O.S. Selections, and the Learning Resources plaintiffs filed for certiorari before judgement was entered in their favor. The cases were consolidated into the one we examine today.

Constitutional Allocation of Tariff Power

The Constitution assigns primary responsibility for tariff policy, along with most other powers related to trade, to Congress. Article I grants Congress the power to “lay and collect Taxes, Duties, Imposts and Excises,” as well as the power to regulate foreign and interstate commerce. Since the founding of our nation, duties on imported goods were understood to fall within the core of Congress’s fiscal and commercial responsibilities. Because tariffs generate federal revenue and shape foreign economic policy, they occupy a central place in the Constitution’s delegation of legislative power.

The Supreme Court has long recognized the structural importance of Congress’s control over revenue mechanisms. The taxing power, the Court said in Gibbons vs. Ogden (1824), “very clearly" includes the power to impose tariffs. James Madison, in The Federalist No. 48, proclaims that the Framers “gave Congress alone…access to the pockets of the people.” Tariffs, as a form of taxation on imported goods, therefore implicate one of Congress’s central and most powerful authorities. Although Congress has periodically delegated limited tariff authority to the executive, such delegations have been explicit and accompanied by significant restraints. This was first addressed in J.W. Hampton vs. United States (1928), when a unanimous Court held that Congress, within “defined limits,” may vest discretion in the executive to adjust public regulations and direct statutory execution. Following this precedent, modern trade statutes authorizing executive tariff adjustments typically specify the conditions under which they may be imposed, and often include procedural safeguards or strict limits.

Enacted in 1977, the International Emergency Economic Powers Act authorizes the President to deal with any “unusual or extraordinary threat” which originates “in whole or substantial part outside the United States” following the declaration of a national emergency. The statute permits the president to act when such a threat affects the nation’s economy, national security, or foreign policy, delegating to the President the ability to act quickly during foreign economic crises while requiring formal emergency declarations and reporting to Congress. Once invoked, IEEPA grants the president authority to investigate, regulate, or otherwise prohibit a large range of financial and commercial transactions involving foreign interests, including freezing assets subject to U.S. jurisdiction, restricting transfers of funds or credits, regulating foreign exchange, and prohibiting transactions involving foreign entities or leaders. Since its enactment, presidents have relied heavily on IEEPA to implement sanctions, block assets, and restrict financial transactions between foreign governments, terrorist organizations, cybercriminals, and other designated targets. Despite the breadth of the statute's authorities, IEEPA has functioned primarily as a sanctions and financial-control statute rather than a mechanism for altering trade policy, and presidential actions have typically targeted specific foreign actors or transactions rather than imposing duties on general imported goods. Against this historical backdrop, President Trump’s invocation of IEEPA to impose broad tariffs was destined to raise significant questions regarding the scope of authority Congress delegated.

The Major Questions Doctrine

In recent years, the Court has developed a test that has come to be known as the major questions doctrine. Formally introduced in 2022, the major questions doctrine requires an executive agency to identify clear congressional authorization before permitting that agency to exercise powers of vast political and economic significance. When an asserted authority would substantially expand the scope of executive power, or reshape a significant sector of the economy, the Court is hesitant to defer to broad statutory language, and thus, requires explicit authorization from the legislature.

Under the Biden Administration, the Court applied the major questions doctrine in a number of high-profile cases regarding sweeping executive action. In West Virginia vs. EPA (2022), the Court rejected the EPA’s interpretation of the Clean Air Act, which would have transformed the nation’s energy production methods. The Court found that this regulation was a “major question,” and emphasized that Congress must “speak clearly” when authorizing decisions of such magnitude. Similarly, in NFIB vs. OSHA (2022), the Court invalidated a nationwide COVID-19 vaccine mandate, concluding that the agency’s authority is limited to workplace safety, not public health. The Court determined that the mandate acted as a major question that required a clear, explicit authorization from Congress rather than a broad interpretation of their emergency powers. More notably, however, was the application of the major questions doctrine in Biden vs. Nebraska (2023). Here, the Supreme Court struck down the Department of Education’s initiative to cancel more than $430 billion in student loan debt, citing authority from the HEROES Act to do so. The Supreme Court held that the Secretary of Education lacked clear congressional authorization to enact such a massive, economically significant policy. Again, the Court affirmed that when the executive branch looks to exert expansive power, it cannot survive unless explicit congressional authorization exists.

The Court’s Decision

If the length of the statutory and doctrinal background is any indication, the dispute in Learning Resources did not arise in a precedent vacuum. Rather, the case sits at the intersection of decades of congressional delegation, evolving presidential emergency declaration practice, and the Supreme Court’s recent efforts to curb the expansion of executive power. Against this relatively recent, but particularly dense backdrop, the Court turned to the central question: Does IEEPA authorize the President to impose tariffs? No. The Court held that IEEPA does not authorize the President to impose tariffs. Although IEEPA does grant the president vast, but explicit, authority to regulate international economic transactions following the declaration of a national emergency, it does not delegate the power to impose duties on imported goods. Because the challenged tariff program represented a core exercise of power vested in Congress, the Court required the Trump administration to point to explicit congressional authorization, and they could not.

The Court began its analysis by applying the major questions doctrine. It emphasized that the President’s tariff program carried significant economic and political consequences, affecting a substantial share of international trade and imposing considerable costs on businesses and consumers. The asserted authority, the Court explained, would constitute a “transformative expansion” of executive control over tariff policy, an area historically subject to congressional control. In such circumstances, this exercise of power represented a major question, and thus, put the burden on the executive to point to explicit congressional authorization to tariff under IEEPA. In explaining their rationale, the Court stated “We have long expressed reluctance to read into ambiguous statutory text extraordinary delegations of Congress’s power.” Drawing on precedent from major questions cases during the Biden administration, the Court reasoned that “Congress would not have delegated highly consequential power through ambiguous language.”

The government contended that IEEPA’s authorization to “regulate” importation encompassed the power to impose tariffs. The Court rejected this interpretation, noting that the statute made no reference to tariffs, taxation, or duties, despite Congress’s consistent practice of using explicit language when delegating tariffing authority in other statutes. Chief Justice Roberts, writing for the majority, stated “when Congress grants the power to impose tariffs, it does so clearly and with careful restraints. It did neither here.” The Court further reasoned that the government could not identify a statute in which a general power to regulate had been understood to mean the power to tax. Interpreting IEEPA to authorize tariffs, then, would allow the executive to exercise a core legislative power based on ambiguous language.

The Court then turned to the historical function of IEEPA, and how it has been invoked by the President’s predecessors. Since IEEPA was passed, Presidents have invoked the statute to address threats from foreign nations by imposing sanctions, freezing assets, and restricting financial transactions. Never, though, had a President used it to impose tariffs. The absence of any precedent for invoking IEEPA to impose tariffs, the Court explained, provided the backdrop for the Court’s reluctance to confer this power to the President. Ultimately, the Court ruled that IEEPA’s grant of authority to “regulate…imports” falls short of including the power to impose tariffs. That power, the Court determined, lies with Congress, and the President could not point to explicit congressional authorization that delegated the tariffing power to him.

Implications of the Decision

The Court’s decision rendered roughly $175 billion dollars of Treasury revenue void, according to A&O Shearman. Evidently, this will raise significant legal issues for both the government and importers, who will be seeking refunds on tariffs paid to the federal government. Shortly after the decision, President Trump signed an executive order directing agencies to immediately stop collection of IEEPA tariffs. Next, the administration moved to replace IEEPA tariffs with a blanket 10% tariff on all imports under Section 122 of the Trade Act of 1974.

For importers, the decision establishes a clear pathway to receiving refunds tariffs paid under IEEPA; but a clear pathway doesn’t necessarily make it a short one. As many as 300,000 companies have applied for refunds through the Court of International Trade, and the Trump administration warns that litigating each case could take years. The scale and speed of the refund process signals broader institutional consequences of the Court’s decision. By invalidating the tariff program that had generated hundreds of billions in revenue, and fundamentally altered corporate fiscal plans, the ruling immediately disrupted both federal fiscal policy and private economic reliance, proving how consequential major questions decisions can be.

Conclusion

In short, Learning Resources marks yet another significant extension of the major questions doctrine into the realm of trade and presidential emergency economic authority. By holding that IEEPA does not authorize presidential imposition of tariffs, the Court squarely asserted that the power to tax belongs to Congress; and any attempt by the executive to exercise core legislative powers must follow an explicit congressional authorization. At the same time, President Trump’s rapid use of alternative statutory authority to impose his tariffs underscores an integral feature of separation-of-powers doctrine: while the major questions doctrine might serve to curtail executive encroachment on congressional authority, the scope of the President’s power ultimately lies in the breadth of authority Congress chooses to delegate.

Avery Sneed is a junior majoring in political science.

Sources

Biden v. Nebraska, 600 U.S. 477 (2023)

Gibbons vs. Ogden, 22 U.S. 1 (1824)

J.W. Hampton, Jr. & Co. v. United States, 276 U.S. 394 (1928)

Learning Resources, Inc. v. Trump, 607 U.S. ___ (2026)

United States. International Emergency Economic Powers Act. 50 U.S.C. §§ 1701–1706.

West Virginia v. Environmental Protection Agency, 597 U.S. 697 (2022)